A strong hiring streak—and the revisions make it even stronger

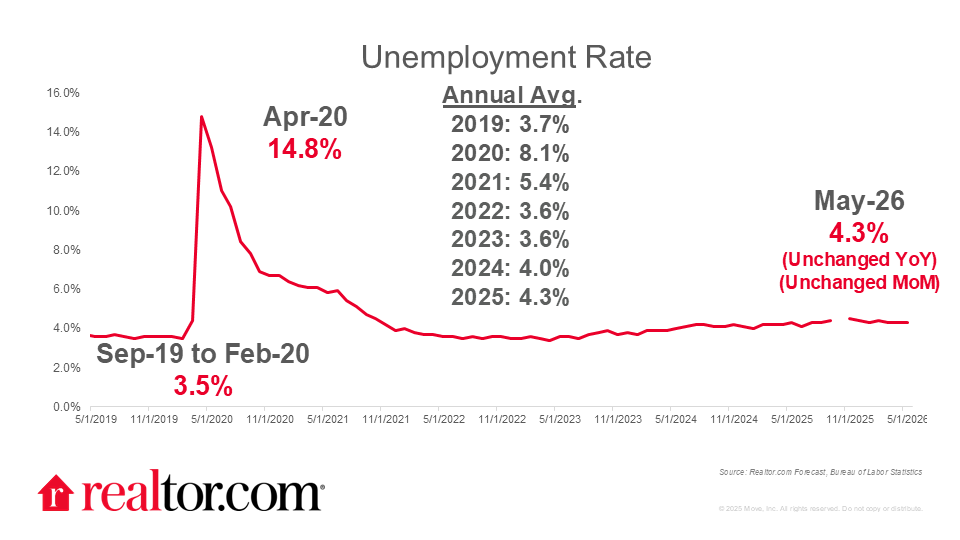

Friday’s jobs report painted a picture of labor market stabilization, and against the current economic backdrop, that’s no small thing. The economy added 115,000 nonfarm payrolls in April, beating consensus forecasts ranging from 55,000 to 70,000. Meanwhile, the unemployment rate held steady at 4.3%. On wages, the 3.6% year-over-year gain is running slightly above CPI and PCE, a relief after months of worry that workers were losing real purchasing power. Still, we’ll know more after next week’s inflation read for April.

The bottom line: After months of choppy prints and last year’s worries about deterioration, the labor market is showing signs of stabilizing. In the months ahead, the labor market needs to crawl before it walks, and walk before it runs.

Good news for the Fed: One fewer fire to put out

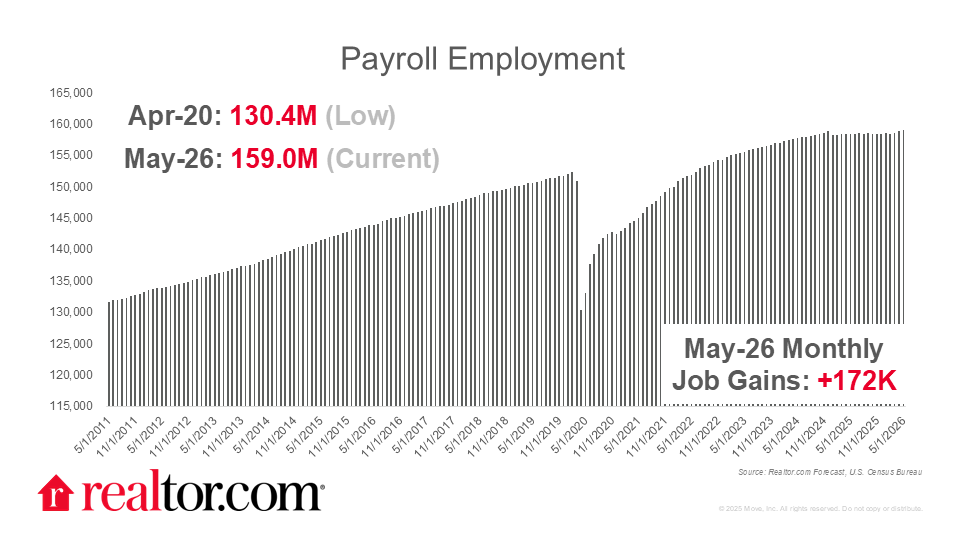

May’s jobs report delivered a third straight month of solid payroll growth, adding 172,000 jobs, which was well above forecasts ranging from 85,000 to 110,000. Unemployment held steady at 4.3% for a third consecutive month. We remain in a low-hire, low-fire labor market, but one that looks increasingly stable. The one risk flagged heading in—that April and March’s strong numbers might get revised down—turned out to be a false alarm. It was quite the opposite, in fact: Combined revisions added 93,000 jobs to those two months, making an already strong stretch of job growth even stronger.

The number that matters most for housing isn’t the headline

For consumers and the housing market, four months of solid job growth is nothing to sneeze at, despite existential questions about how AI might reshape the labor market in the coming years. However, the statistic that matters most for households and housing is not the headline jobs figure: It is the race between earnings growth and inflation.

Average hourly earnings rose 3.4% year over year in May, slipping from 3.6% last month—and with CPI expected around 4.2% when it lands next week, real wages remain negative and are moving in the wrong direction. So far this spring, housing demand has stayed resilient, with annual gains in pending listings and contract signings. Sellers are reading the market better than last year, and asking prices have fallen for seven straight months. But despite some buyer-friendly momentum, the headwinds—elevated rates, inflation, and uncertainty—are substantial. For the housing market to keep treading water, we need the labor market to hold or, ideally, show signs of a real summer pickup.

Subscribe to our mailing list to receive updates on the latest data and research.

{kind=link}