The U.S. labor market took center stage last week as three major labor market indicators outperformed forecasts. Robust payroll additions in both the public and private sectors, paired with a massive surge in job openings, point to a workforce on solid footing. However, this momentum has complicated the inflation outlook, ending the S&P 500’s nine-week winning streak as markets recalibrate to the reality of higher-for-longer interest rates.

Labor Market Resilience: May Employment Data

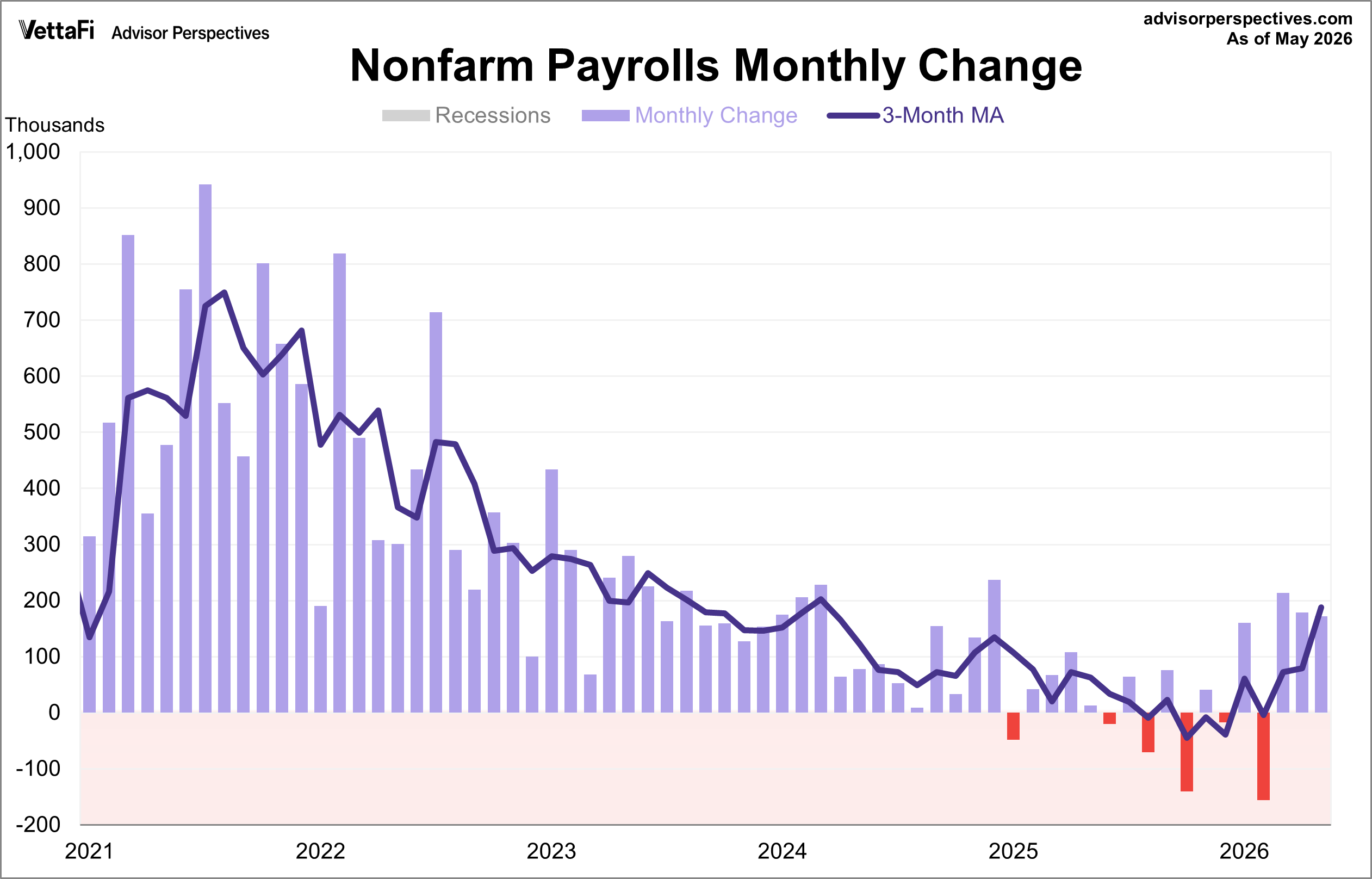

The U.S. labor market maintained its resilience in May, with job gains more than doubling expectations. The Bureau of Labor Statistics reported the economy added 172,000 jobs last month, outpacing the projected 80,000. Additionally, job gains for the previous two months were revised upwards, with April’s figure now at 179,000 and March’s at 214,000. Momentum appears to be building in the labor market, as this represents the largest three-month expansion in over two years and the longest streak of monthly growth in a year. Meanwhile, the unemployment rate held steady at 4.3%, as expected.

Private Sector Momentum: ADP Employment Report

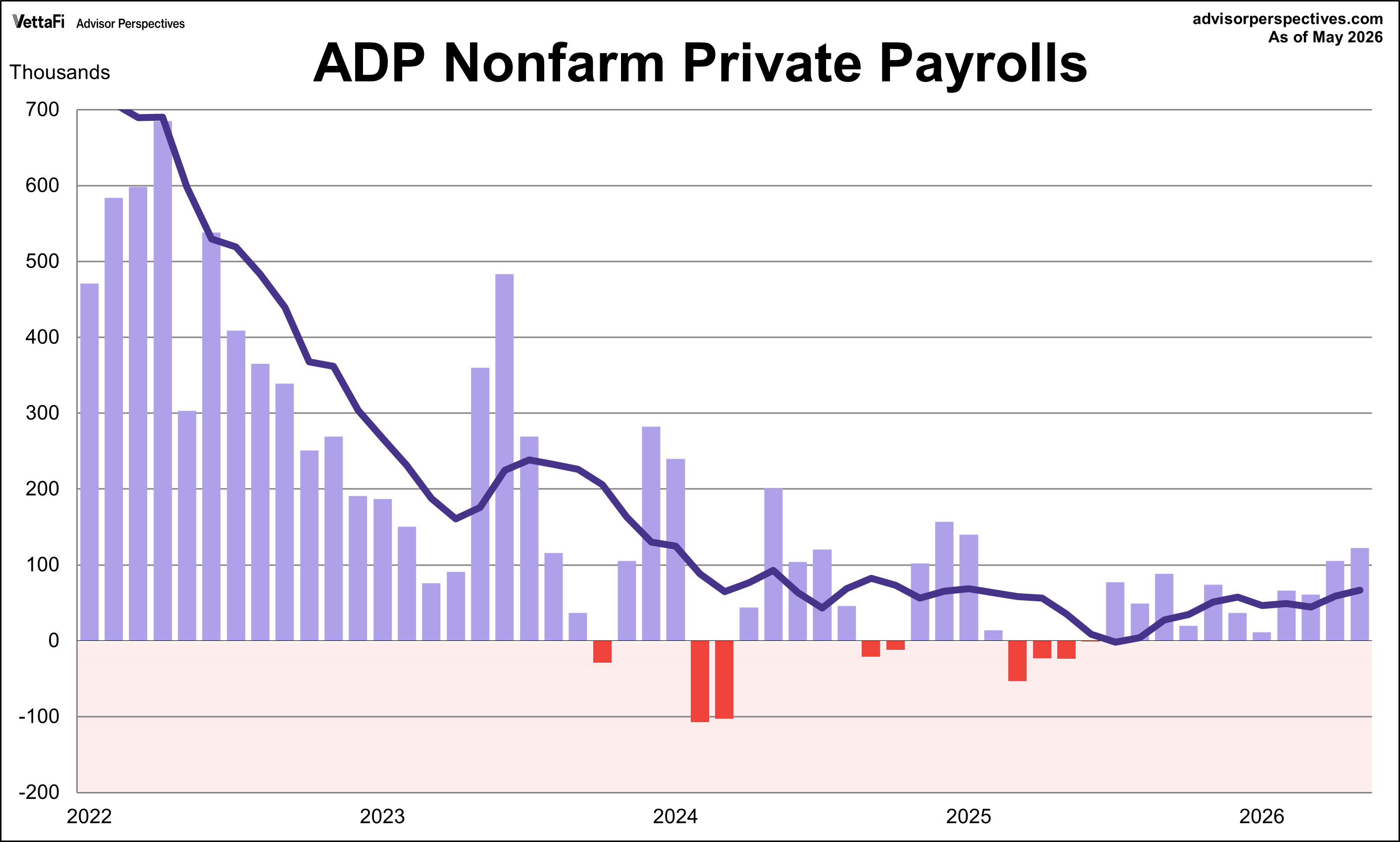

The May ADP National Employment Report offered further evidence of a healthy U.S. labor market, as private sector payrolls also surprised to the upside by adding 122,000 jobs, coming in above the projected 118,000. This figure represents the strongest monthly gain since January 2025 and marks the eleventh consecutive month of expansion for the private sector, the longest streak in nearly three years.

Although gains were widespread across nearly all industries, Education and Health Services accounted for nearly half the total, adding 57,000 jobs. Additionally, growth occurred across companies of all sizes but was most notable among small (1–19 employees) and large (500+ employees) employers, which contributed a combined 89,000 jobs.

Job Openings and Labor Turnover: April JOLTS Summary

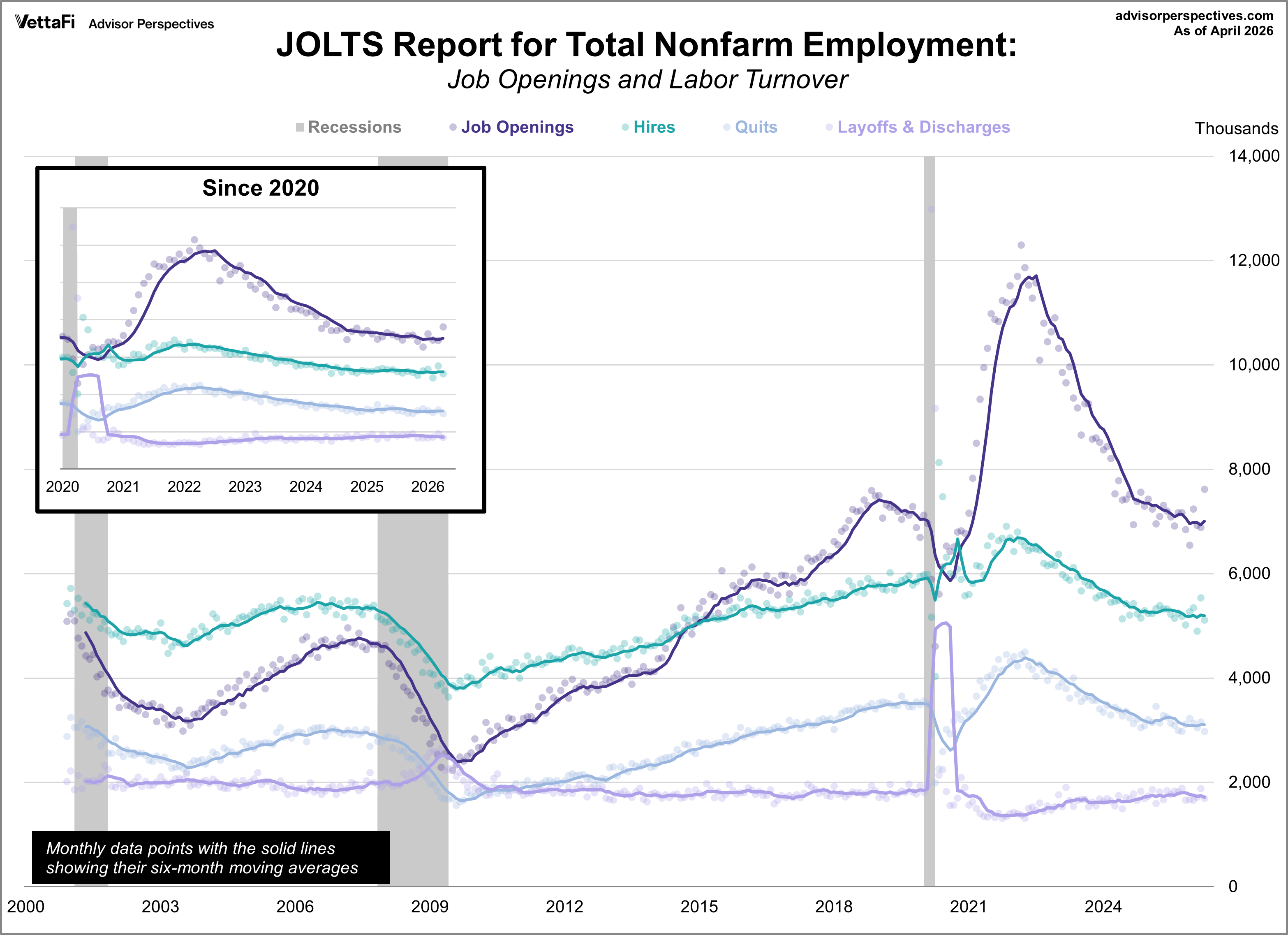

April’s JOLTS report reinforced the narrative of a solid labor market as job openings reached their highest level in nearly two years. Vacancies surged by 731,000 to 7.618 million, marking the largest monthly increase since 2021 and landing well above the expected 6.860 million. This jump pushed the ratio of job openings to unemployed workers to 1.03, its highest level in over two years and marking the first time since last June that available positions outnumbered job seekers.

In contrast to the spike in vacancies, actual labor turnover slowed down. April saw simultaneous declines in hires, layoffs, and quits, with quits reaching a multi-year low as worker confidence cooled. This lack of movement suggests the market remains in its ‘low-hire, low-fire’ holding pattern that characterized most of 2025.

Market Reactions and Fed Outlook

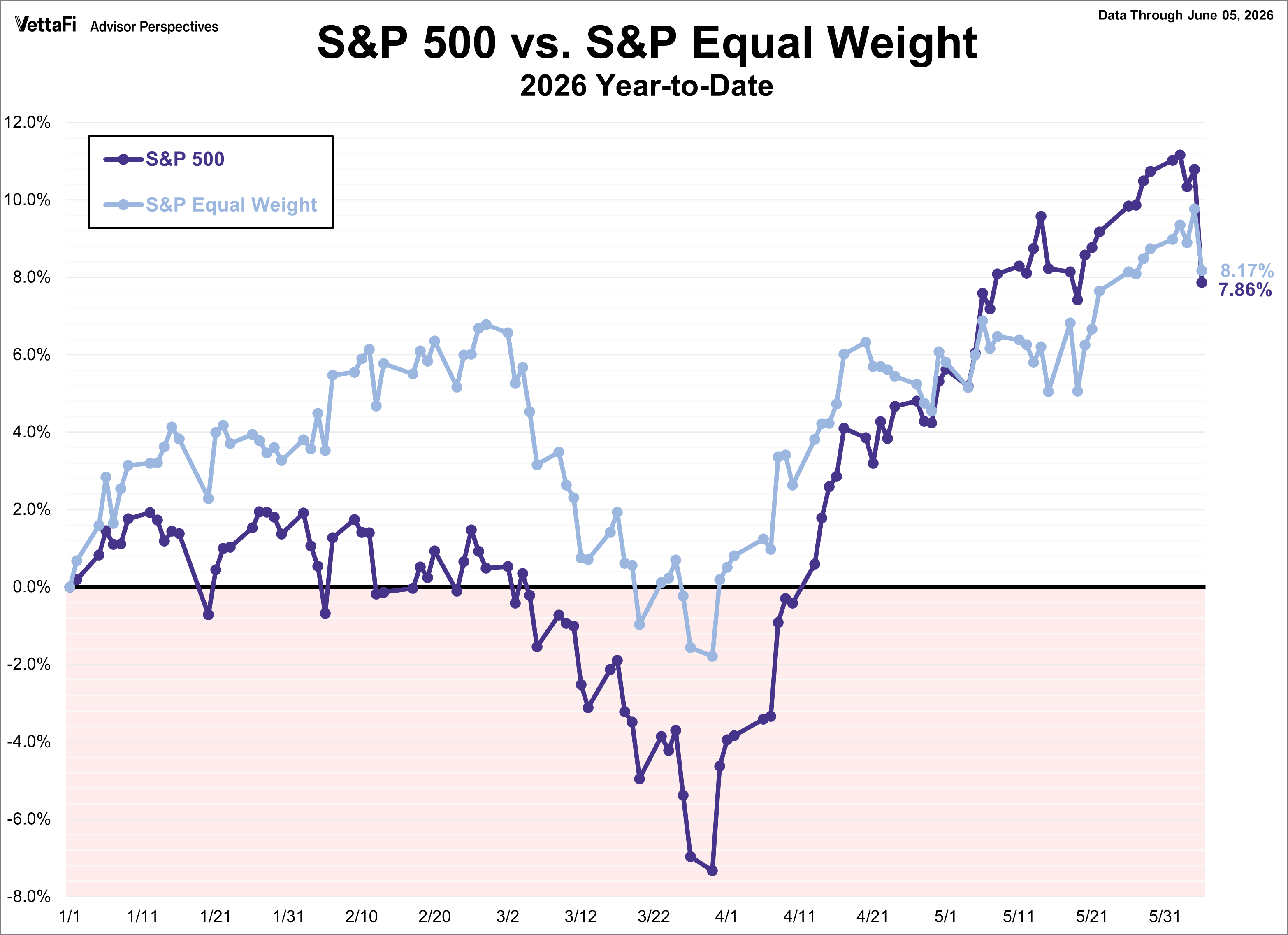

Although the S&P 500 reached multiple record highs early last week, its upward momentum was halted on Friday by the stronger-than-expected jobs report, which triggered the index’s largest single-day drop since April 2025. This sharp plunge served as the primary driver behind the 2.6% weekly loss, ultimately snapping the index’s nine-week winning streak. As a result, the SPDR S&P 500 ETF Trust (SPY) fell 2.5% last week. Meanwhile, the S&P Equal Weight Index was down 0.5% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell 0.5%.

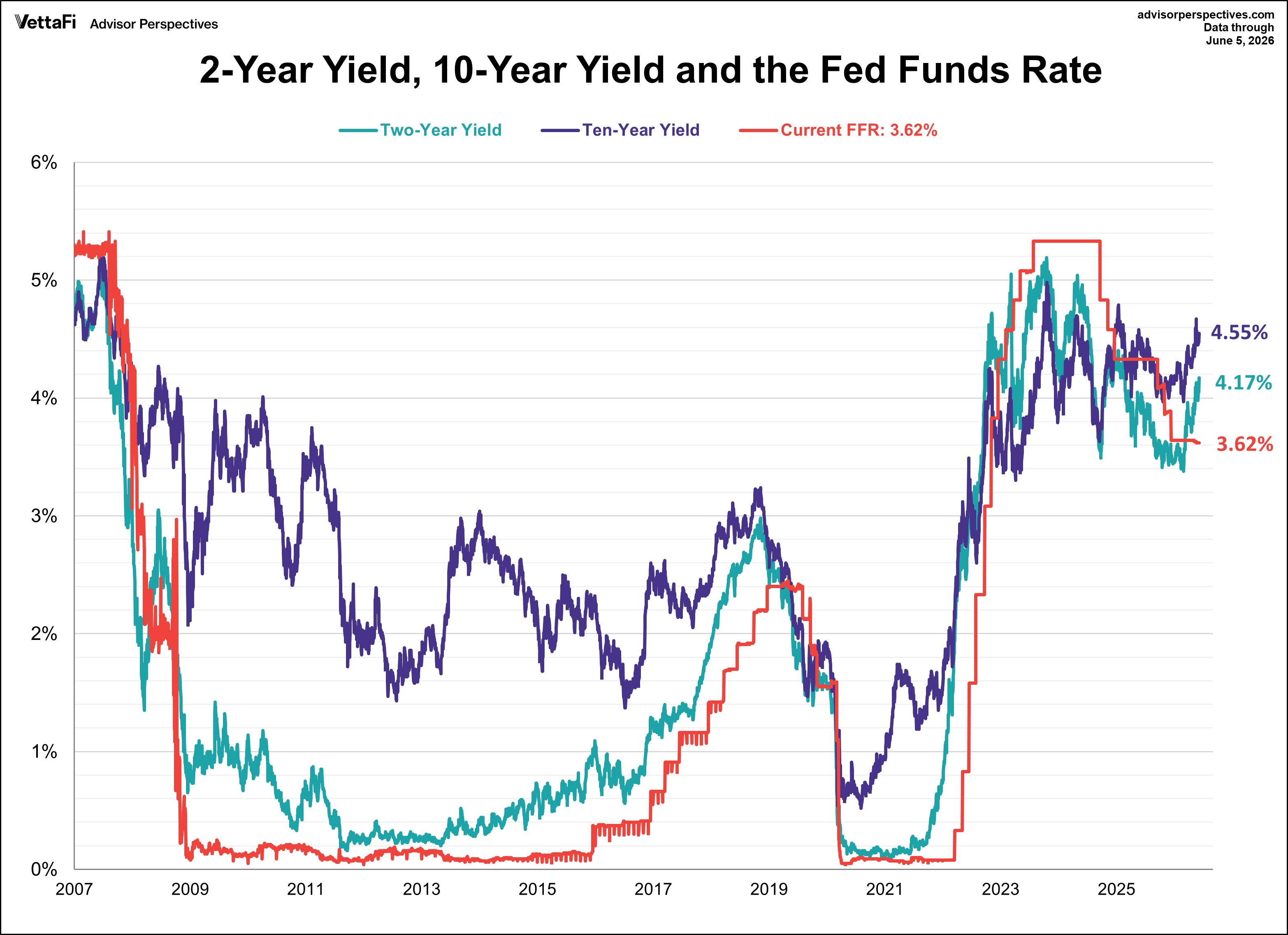

The 10-year Treasury yield finished the week at 4.55%, while the 2-year note finished at 4.17%, its highest level since February 2025.

With the labor market demonstrating standalone strength, the Federal Reserve can shift its primary focus to inflation, positioning a rate hike as a probable next step. The CME FedWatch Tool currently shows a 96% likelihood that the Federal Reserve will hold rates steady at its meeting next week, versus a 4% chance of a cut. Markets are currently pricing in a 25 basis point hike by the end of 2026 followed by a pause through all of next year.

Looking Ahead: Economic Data for the Week of June 8, 2026

- Monday: No notable data

- Tuesday: NFIB Small Business Optimism Index (May), Existing Home Sales (May), Trade Balance (Apr), Short Term Energy Outlook (June)

- Wednesday: Consumer Price Index (May)

- Thursday: Weekly Jobless Claims, Producer Price Index (May)

- Friday: University of Michigan Consumer Sentiment Index (June)

Originally published on Advisor Perspectives

For more news, information, and strategy, visit ETF Trends.

{kind=link}